by Brad Anderson

- BYD, Changan, Chery, and Geely together account for over half of China’s car sales.

- Startups like Nio, Xpeng, and Xiaomi remain independent but face rising pressure.

- Many Chinese car brands are unlikely to survive through the next ten years.

Do you struggle to wrap your head around China’s car market and the dizzying number of brands that it is home to? If so, then this detailed infographic aims to make the nation’s automotive industry a little easier to understand. Though be warned, studying it might leave you with just as many questions as answers.

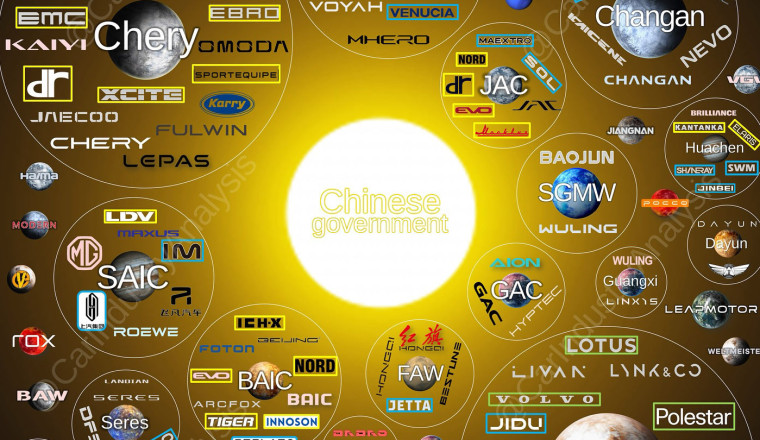

This chart, compiled by industry analyst Felipe Munoz, lays out every carmaker currently owned fully or partially by Chinese firms. In terms of sales, the four biggest groups in the country are Geely, BYD, Chery, and Changan. The last two stand out in particular, as they are both state-owned.

Who Owns What?

Among the brands found within the Chery group are Fulwin, Omoda, Jetour, Exeed, iCar, Luxeed, Jaecoo, Rely, and of course the Chery brand itself. Within Changan you will find Avatr, Deepal, Nevo, Volga, and Kaicheng.

Then there’s Geely. Brands it owns either fully or in part include Zeekr, Proton, Farizon, LEVC, Galaxy, Volvo, Lotus, Lynk & Co, Polestar, Smart, Geome, Belgee, and Radar. By comparison, BYD’s portfolio is quite more simple, consisting of its namesake brand alongside Denza, YangWang, and Fan Cheng Bao.

Read: China’s EV Fire Fix Shoots Battery Into Traffic And Makes It Their Problem

As noted by Munoz, these four groups account for 56 percent of all Chinese car sales. All of them receive subsidies from the local government, and in this chart, the companies located closest to the sun are the ones with the most state involvement.

The Wider Circle

Beyond China’s Big 4, other important conglomerates include SAIC, which owns the MG, LDV, Maxus, IM, and Roewe brands, JAC which owns Maextro, JAC, Evo, and Nord, as well as BAIC, which includes Arcfox, Foton, Tiger, and Stelato. There’s also Dongfeng, which owns the MHero, Voyah, Lingxi, Nammi, and Venucia brands.

There are also several notable startups that have so far avoided being gobbled up by one of the big groups. These include Nio, which has gone on to launch the Onvo and Firefly brands, Leapmotor, Xpeng, Aiways, Neta, Xiaomi, Li Auto, and Rox.

Stacking China’s Car Brands By Status

Separately, Munoz’s also shared a second chart on Instagram with a pyramid that shows how 109 brands align by market position. At the peak sit ultra-premium names like Hongqi, YangWang, and Maextro. One level down are high-tech challengers such as Xiaomi, Nio, and Li Auto.

Below that, the premium and semi-premium tiers are crowded with names like Stelato, Denza, Zeekr, and Xpeng, all targeting status-conscious buyers. The base is packed with older, budget-focused marques that remain little-known in the West, including Sinogold, Hima, Pocco, and several others. These brands risk slipping into obscurity as consumers increasingly turn toward more advanced, connected vehicles.

Survival Of The Fittest

All that being said, it’s highly unlikely that all of these brands will still be around 10 years from now. While the big groups should stick around, they may choose to combine some of their sub-brands or ditch them altogether, a pattern long familiar in the West with names like Pontiac, Oldsmobile, NSU, Autobianchi, Sunbeam and hundreds of other brands disappearing from showrooms over the decades.

What’s crystal clear is that Chinese car manufacturers aren’t going anywhere and will continue to play an important role in the global industry for years to come.